2025 M&A Industry Update

As we navigate through 2025, the M&A landscape within the AEC industry continues to evolve. We sat down with Chief Acquisition Officer Aaron Tippie, PE and Director of Mergers & Acquisitions Trevor Garfield to discuss the current trends, challenges, and strategies shaping our approach to mergers and acquisitions.

Q: What are the current trends in the M&A industry?

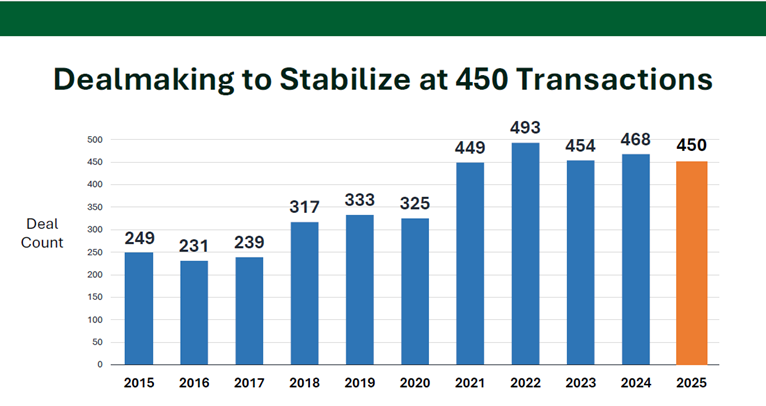

AT: The AEC industry is witnessing a continued high number of transactions, with certain forecasts suggesting around 450 deals will be done in 2025. While this year’s activity may not surpass the 493 transactions of 2022, it’s still indicative of an industry enjoying a high level of investor interest. In particular, private equity's (PE) involvement in the space continues to increase, whether as a pure play investor or sponsor of a strategic acquirer. The largest AEC firms are increasingly backed by PE. And, given that over half of firms actively held by private equity are approaching several years of maturity within their hold period, more of those firms will soon be returning to the market as new investors are sought. This presents a great opportunity for well-capitalized buyers to partner with strong companies that have been otherwise unavailable in recent years.

Figure 1: Annual M&A deal volume in the AEC industry remains near record highs, with 2025 projected to see around 450 transactions. (Source: Morrissey Goodale M&A Deals Database)

TG: I agree. The AEC industry has continued to see private equity involvement rise, which inundates our space with capital and strategic resources. This raises the tide of sophistication across our industry, creating firmer competition when trying to grow a business either organically or inorganically. The challenging question to answer is how all this PE involvement impacts Westwood's purchasing of other businesses, and which industry segments will see the most activity.

Q: Which industry segments are seeing the most activity?

AT: The hottest industry segments for M&A include transportation, water and wastewater, and nearly anything energy or power related, which drives a lot of interest and therefore higher prices. Many other segments of AEC remain great areas for investment, enabling continued growth of a diversified platform at much more reasonable prices.

TG: To build on what Aaron is describing, the public markets have felt downward pressure since historic valuation highs in 2022 that sustained through the end of 2024. Currently, the valuation of public AEC firms has seen a 25% decrease since November 2024. While this seems like a big decrease, the public market is still at a healthy, sustainable valuation (the decrease is pegged to all-time highs). However, this decrease has pushed the market to pick and choose where they want to 'lean in' when purchasing an asset. Firms are paying very high premium pricing for businesses with access to the end markets most likely to outperform when there is volatility in the broader macro-environment. This is how we get the answer to your question: pricing pressure leads to pricing competition in certain industries for certain firms. These firms focus on power (T&D, substation), water/wastewater, aviation, and, to a lesser extent, transportation. At the other end of the spectrum, we are seeing a stabilization of valuation in assets that are more heavily tied to privately funded new construction projects, like land development-focused firms.

Q: Have there been any surprises in M&A activity this year?

AT: For some marketed processes, the sheer number of bidders involved and the incredibly high prices being offered for certain firms, despite actual performance of the business, soundness of strategy, or quality of leadership. This is often specific to the "hottest" industry segments mentioned above.

TG: I concur. Marketed processes remain incredibly crowded, and valuations for certain firms are sky-high. This is nothing new. M&A at Westwood continues to operate as a well-oiled machine, and I continue to be impressed by our ability to stay disciplined, focused, and culture-first when approaching M&A. We have a great team, and we continue to find great firms like CSRS, a Westwood company, that can uniquely position our firm to outperform culturally and operationally.

Q: How have recent economic, political, and regulatory conditions impacted M&A activity?

AT: Short-term economic uncertainty can influence firms' decisions on when to sell. We've observed some hesitance among private equity portfolio companies nearing the end of their hold period. Regulatory changes that result in a cooling of renewable energy implementation could have a near-term effect of reducing demand and therefore the price of firms with significant exposure to those markets.

TG: Time will tell. Short-term uncertainty can impact the decision matrix of firms relating to when they should sell. We have seen some of this on occasion with private equity portfolio companies that are “long in tooth” or nearing the end of their hold period. If anything, we are seeing inflation normalize and wage increases taper off after a long period of record-high increases. This is healthy for businesses and can be helpful from a fundamental valuation standpoint.

Q: How is our organization adapting to the evolving M&A landscape?

AT: We are being more deliberate about investing in creating relationships, in person, early in the process. Spending meaningful time with people is the fastest way to build trust, understanding, and set the path for a new partnership. Said another way, we are carefully cultivating relationships. Contrary to adapting to very quick, sometimes rash, movements in the market, maintaining fiscal and strategic discipline within certain corners of the industry will serve Westwood well in the long run.

TG: We want to be consistent, deliberate, and disciplined. Relationships and culture are still number one. We want to form meaningful relationships with the firms we are pursuing. This takes time and must be prioritized in order for it to be successful. So far, so good.

Q: What strategies is Westwood implementing to stay competitive in the M&A market?

AT: We are maintaining our genuine focus on investing in great leaders, compatible cultures, high-performing teams, and alignment of vision and strategic goals. This means saying no to many potentially viable deals, even if they work "on paper." Enabling business owners to speak directly with leaders who have joined Westwood via acquisition, in an unscripted and unfiltered environment, provides great credibility for our philosophy and approach. Our relationship with Blackstone can be incredibly helpful in making introductions and certainly provides a high level of credibility and proven performance among the community of PE-backed strategic buyers.

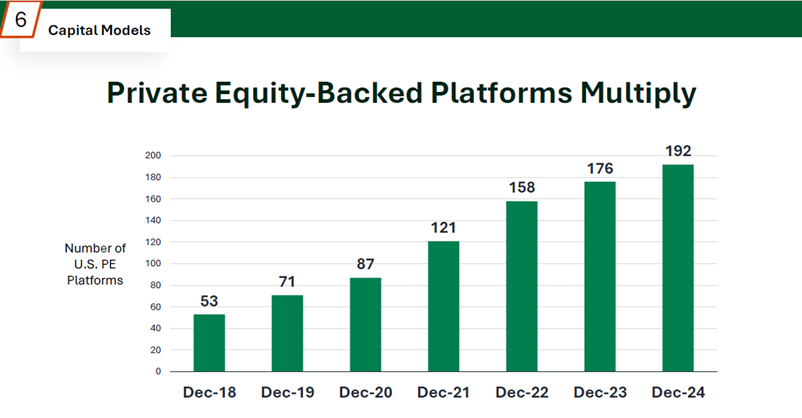

Figure 3: The number of PE-backed platforms in the U.S. AEC sector has more than tripled since 2018. (Source: Morrissey Goodale)

TG: What Aaron is describing is critical. Leadership and culture come first. If we are aligned on the desired outcome for our collective firms and want the best possible outcome for our clients and our people, then we can meaningfully cultivate connections with the firms we pursue. This is essential for long-term success.

Q: What insights do industry experts have regarding the future of M&A?

AT: M&A will continue to occur at a high volume for the foreseeable future as the AEC industry overall remains ripe for consolidation, with 10,000 firms in North America. The industry offers strong returns across multiple end markets, a continued runway for industry growth based on large-scale infrastructure needs and new business opportunities, and the increasing rate of PE investment and successful exits.

TG: With the high volume Aaron is describing, we’ll continue to see healthy valuation across the board with some outlier valuations in specific sectors. As we talked about earlier, the buyer universe within our M&A landscape is laser-focused on assets that drive accretive growth and is willing to pay up for those assets.

Q: What is the focus of our M&A team for the remainder of 2025?

AT: Our team will concentrate on supporting our recent integration while identifying and pursuing other partnerships across markets and geographies most complementary to Westwood's current business portfolio. Additionally, we are laying the foundation for acquisitions that may occur beyond 2025, as some partnerships require a longer investment of time.

Conclusion

As we move forward in 2025, Westwood remains committed to navigating the complexities of the M&A landscape with a disciplined approach. By focusing on relationships, maintaining strategic priorities, and adapting to market conditions, we are well-positioned to continue our growth and success in the AEC industry. With the continued support of our partnership with Blackstone and our proven track record of successful integrations, we look forward to identifying partnerships that will strengthen our position in the market while staying true to our culture-first philosophy.